Haryana State Board HBSE 10th Class Social Science Solutions Economics Chapter 3 Money and Credit Textbook Exercise Questions and Answers.

Haryana Board 10th Class Social Science Solutions Economics Chapter 3 Money and Credit

HBSE 10th Class Economics Money and Credit Intext Questions and Answers

Let’s Work These Out (Page No. 40)

Economics Chapter 3 Class 10 Question Answers HBSE Question 1.

How does the use of money make it easier to exchange things ?

Answer:

Money acts as an intermediate in the exchange process. It is called a medium of exchange. Money has eliminated the problem of double co-incidence of wants, as in the barter system.

Class 10 Economics Chapter 3 Questions And Answers HBSE Question 2.

Can you think of some examples of goods/services being exchanged or wages being paid through barter?

Answer:

Yes, in rural areas of our country, goods/services are being exchanged or wages being paid, through barter. In rural areas, food grains are exchanged without the use of money. The peasants are given wages in the form of commodities, not in cash. This commodity may be wheat, rice, millet or any other goods.

![]()

Let’s Work These Out (Page No. 42)

Money and Credit Chapter 3 HBSE 10th Class Question 1.

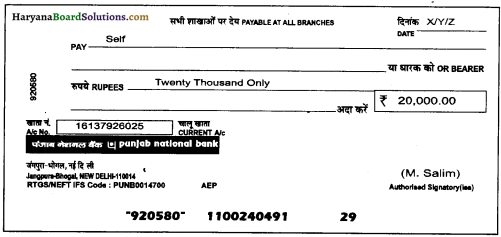

M. Salim wants to withdraw Rs 20,000 in cash for making payments. How would he write a cheque to withdraw money?

Answer:

First of all, M. Salim would write the concerned date, on the given place, on the cheque. He would instruct the bank to pay ‘Self.’ Then, he would write ‘Twenty Thousand Rupees only’ against rupees printed on the cheque and would fill the amount and account number, in their corresponding boxes, given on the cheque. Further, M. Salim would sign on both sides of the cheque, i.e. at the place of signature and backside of the cheque and then, he would submit it on the withdrawal counter of the Bank to get cash from the cashier.

Question 2.

Tick the correct answer :

After the transaction between Salim and Prem,

Salim’s balance in his bank account increases and Prem’s balance also increases.

(ii) Salim’s balance in his bank account decreases and Prem’s balance increases.

(iii) Salim’s balance in his bank account increases and Prem’s balance decreases.

Answer:

(ii) Salim’s balance in his bank account decreases and Prem’s balance increases.

Question 3.

why are demand deposits considered as money?

Answer:

Demand deposits are considered as money because people have a choice to withdraw money through cheques or withdrawal slips.

![]()

(Page No. 42)

Question 1.

What do you think would happen if all the depositors went to ask for their money at the same time ?

Answer:

If all the depositors went to ask for their money at the same time, the bank will not be able to give all the depositors their money. The reason is, that, the banks would have used the major portion of the deposits to extend loans.

Let’s Work These Out (Page No. 44)

Question 1.

Fill the following table:

| Salim | Swapna | |

| Why did they need credit ? | ||

| What was the risk ? | ||

| What was the outcome ? |

Answer:

| Salim | Swapna | |

| Why did they need credit? | To meet the working capital needs of shoe production. | To meet the expenses of cultivation. |

| What was the risk? | Not delivering the order on time. | Failure of crop. |

| What was the outcome? | Able to deliver the order on time, make a good profit and repay the loan. | Caught in debt trap and had to sell a part of her land to repay the loans. |

Question 2.

Supposing Salim continues to get orders from traders. What would be his position after 6 years?

Answer:

If Salim continues to get orders from traders, then after 6 years, he will be in a good financial position. Then, he will have no need to take a loan and he might extend his business.

Question 3.

What are the reasons that make Swapna’s situation so risky? Discuss factors pesticides, role of moneylenders, climate.

Answer:

The reasons for Swapna’s situation being risky are –

(i) Failure of crop due to either poor rainfall (Climate Problem) or attack on the crop by pests. Pesticides will reduce or eliminate the attack by pests and good rainfall will eliminate the risk due to climate.

(ii) Here the role of moneylenders is important because they charge high-interest rates and also will take away part of Swapna’s land if she defaults on loan repayment when her crop fails. This will reduce her earning power even further in the future.

![]()

A House Loan (Page No. 45)

Megha has taken a loan of Rs. 5 lakhs from the bank to purchase a house. The annual interest rate on the loan is 12 percent and the loan is to be repaid in 10 years in monthly instalments. Megha had to submit to the bank, documents showing her employment records and salary before the bank agreed to give her the loan. The bank retained as collateral the papers of the new house, which will be returned to Megha only when she repays the entire loan with interest.

Question

Fill the following details of Megha’s housing loan :

| Loan amount (in rupees) | |

| Duration of loan | |

| Documents required | |

| Interest rate | |

| Mode of repayment | |

| Collateral |

Answer:

| Loan amount (in rupees) | 5,00,000 |

| Duration of loan | 10 years |

| Documents required | employment record and salary record |

| Interest rate | 12% annually |

| Mode of repayment | monthly instalments in cash/by cheque |

| Collateral | the papers ofthe new house |

Let’s Work These Out (Page No. 45)

Question 1.

Why do lenders ask for collateral while lending ?

Answer:

Lenders ask for collateral while lending. This collateral may be land, house, jewellery, vehicle etc. If borrower fails to repay the loan, the lender has the right to sell the collateral, to get back their money.

Question 2.

Given that a large number of people in our country are poor, does it in any way affect their capacity to borrow ?

Answer:

A large number of people in our country are poor. This affects their capacity to borrow. They do not have any collateral security to deposit with the lender. Sometimes, they do not want to borrow money because they know, that they will not be able to repay the loan.

![]()

Question 3.

Fill in the blanks choosing the correct option from the brackets.

While taking a loan, borrowers look for easy terms of credit. This means ………….. (low/ high) interest rate …………. (easy/tough) conditions for repayment ………… (less/more) collateral and documentation requirements.

Answer:

While taking a loan, borrowers look for easy terms of credit. This means low interest rate, easy conditions for repayment, less collateral and documentation requirements.

Let’s Work These Out (Page No. 47)

Question 1.

List the various sources of credit in Sonpur.

Answer:

Following are the sources of credit in Sonpur :

- Village moneylenders

- Agricultural traders

- Banks

- Medium landowners.

Question 2.

Underline the various uses of credit in Sonpur in the above passage.

Answer:

The various uses of credit in Sonpur in the above passage are as follows:

- Shyamal tells that every season he needs loans for cultivation on his 1.5 acres of land.

- Arun is one of the few persons in Sonpur to receive bank loan for cultivation.

- There are several months in the year when Rama is without work and needs credit to meet the daily expenses. Expenses on sudden illness or functions in the family are also met through loan.

Question 3.

Compare the terms of credit for the small farmer, the medium farmer and the landless agricultural worker in Sonpur.

Answer:

Comparison of terms of credit for the small farmer, the medium farmer and the landless agricultural worker :

| Small Farmers | Medium Farmers | Landless Agricultural Workers |

| 1. Interest rate is 60% per annum. | Interest rate is 8-5% per annum. | Interest rate is 60% per annum. |

| 2. No need of collateral and documents. | Required collateral and documents. | No need of collateral and documents. |

| 3. To be repaid when the crops are ready for harvesting and by supplying crops to traders. | Can be repaid anytime in the next three years. | Repaid the money by working for the landowner. |

Question 4.

Why will Arun have a higher income from cultivation compared to Shyamal?

Answer:

Arun will have a higher income from cultivation, compared to Shyamal, because of the following reasons :

- Arun has 7 acres of land, while Shyamal has 1-5 acres of land.

- Arun has received a loan from bank at 8-5 per cent per annum, while Shyamal has received two loans : one, from the village moneylender at 60% per annum and other, from an agricultural trader at 36% per annum.

- Arun can repay the loan anytime, in the next three years, while Shyamal has to repay the loan within 3-4 months.

- Arun is free to sell his crop to anybody, at any price and at any time, while Shyamal has to sell his crop to the moneylender and the agricultural trader, as per his promise.

- Arun has to pay low interest, while Shyamal has to pay high interest.

Question 5.

Can everyone in Sonpur gets credit at a cheap rate ? Who are the people who can?

Answer:

No, everyone in Sonpur cannot get credit at a cheap rate.

The people who have collateral to deposit in the bank and have proper documents, can get credit from banks, at a cheap interest rate.

![]()

Question 6.

Tick the correct answer.

(i) Over the years, Rama’s debt:

(a) Will rise,

(b) Will remain constant,

(c) Will decline.

Answer:

(a) Will rise.

(ii) Arun is one of the few people in Sonpur to take a bank loan because

(a) other people in the village prefer to borrow from the moneylenders.

(b) banks demand collateral which everyone cannot provide.

(c) interest rate on bank loans is same as the interest rate charged by the traders.

Answer:

(b) banks demand collateral which everyone cannot provide.

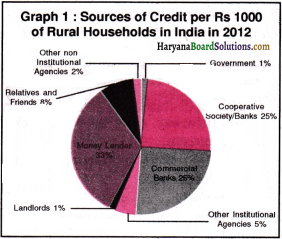

Graph-1 (Page No. 48)

Question 1.

In Graph-1 you can see the various sources of credit for rural households in India. Is more credit coming from the formal sector or the informal sector?

Graph-1: Sources of credit for rural households in India in 2010

Answer:

Credit coming from the formal sector = 56%

Credit coming from the informal sector = 44%.

More credit is coming from formal sector.

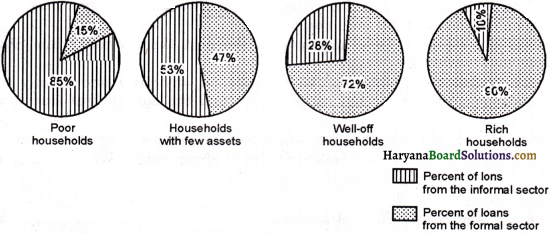

Graph-2 (Page No. 49)

Question 2.

Of all the loans taken by urban households, what percentage was formal and what percentage was informal?

Answer:

| Nature of Household | Informal Source of Credit | Formal Sources of Credit |

| Poor households | 85% | 15% |

| Households with few assets | 53% | 47% |

| Well-off households | 28% | 72% |

| Rich households | 10% | 90% |

Per cent of loans from the informal sector = \(\frac{85+53+28+10}{4}=\frac{176}{4}\) = 44 %

Percent of loans from the formal sector = \(\frac{15+47+72+90}{4}=\frac{224}{4}\) = 56%

Let’s Work These Out (Page No. 50)

Question 1.

What are the differences between formal and informal sources of credit?

Answer:

Following are the differences between formal and informal sources of credit:

Formal Sources:

- Formal sources include banks and co-operative societies.

- They have to follow government rules and regulations.

- RBI supervises the functing of formal sources of loans.

- They provide loan at lower interest rate.

- The purpose of formal sources is profit making, as well as public welfare.

Informal Sources:

- Informal sources include money-lenders, traders, employers, relatives and friends etc.

- Though, they also have government rules and regulations, but they are not followed.

- There is no organisation, which supervises the credit activities of lenders, in informal sector.

- They provide loan at whatever interest rate they choose.

- The purpose of informal sources is only to earn profit.

Question 2.

Why should credit at reasonable rates be available for all ?

Answer:

Credit should be available for all at reasonable rates. Higher cost of borrowing, means, a large part of the earnings of the borrower is used to repay the loan. That’s why, borrowers have less income left for themselves. In certain cases, the high interest rate for borrowing can mean, that, the amount to be repaid is greater than the income of the borrower. This could lead to increasing debt and debt trap. Also, people who might wish to start an enterprise by borrowing, may not do so, because of the high cost of borrowing.

For these reasons, banks and co-operative societies need to lend more. This would lead to higher incomes and many people could borrow cheaply for a variety of needs. They could grow crops, do business, set-up small-scale industries etc. They could set up new industries, or trade in goods. Cheap and affordable credit is crucial for a country’s development.

Question 3.

Should there be a supervisor, such as the Reserve Bank of India, that looks into the loan activities of informal lenders? Why would its task be quite difficult?

Answer:

Yes, there should be a supervisor, such as the Reserve Bank of India, that looks into the loan activities of informal lenders. But, its task would be quite difficult because informal lenders are not registered with government-affiliated, or any other institution. The informal sector of lending money is very wide. Besides, informal lenders have personal relations with borrowers, to get information about such lenders and taking actions against them, would be quite difficult.

![]()

Question 4.

Why do you think that the share of formal sector credit is higher for the richer households compared to the poorer households?

Answer:

The share of formal sector credit is higher for the richer households, compared to the poorer households, because they are more educated than rural people. They are more aware than rural or poor people, about the facilities provided by the government and they know, that banks provide loans at a lower rate of interest. Besides, the rich have collateral security to deposit in the bank against the loan and have proper documents, while the poor do not have such things.

HBSE 10th Class Economic Money and Credit Textbook Questions and Answers

Question 1.

In situations with high risks, credit might create further problems for the borrower. Explain.

Answer:

Yes, it is true that in situations with high risks, credit might create many problems for the borrower, in spite of solving his problems. The credit helps people to increase their earnings, but in some situations, it pushes people into a debt trap. If people are not able to repay the loan, then they have to sell their assets or land, to repay the loan, and if they take the further loans, then they are caught in the hand of debt. Then, the situation of borrowers may be worse off than before.

Question 2.

How does money solve the problem of double co-incidence of wants? Explain with an example of your own.

Answer:

Double coincidence of wants is the most difficult problem of the barter systems. Double co-incidence refers that goods in possession of two different persons must be useful for each other and needed by each other. If wants do not exactly between the two, no exchange will take place. Money solves the problem of coincidence. It acts as an intermediate in the exchange process.

Example – Amit has a spare pair of shoes and wants to buy some wheat and sell shoes. So, it is very difficult for Amit to find such a person who wants his shoes and agrees to solve his problem. Only money is accepted as a medium of exchange, commonly. Now, Amit sells the spare pair of shoes in the market and gets money. After that, he can buy wheat with this money. So, money has solved the problem of double co-incidence of wants.

Question 3.

How do banks mediate between those who have surplus money and those who need money?

Answer:

Banks obtain money from those people who have surplus money, by opening their accounts in the bank and paying them interest on their deposits. On the other hand, banks provide loans to those people who are in need of money. They use a major portion of deposits to extend loans. Banks charge a higher interest rate on loans than what they earn on deposits. The difference between charged and paid interest is the main source of income for banks. In this way, banks mediate between those, who have surplus money (depositor), and those, who need money (borrower).

Question 4.

Look at a 10 rupee note. What is written on top? Can you explain this statement?

Answer:

If we look at a 10 rupee note, we see the following things written on the top –

RESERVE BANK OF INDIA

Guaranteed By The Central Government

I promise to pay the bearer the sum of ten rupees.

This means, that the Reserve Bank of India has a right to issue currency notes, on behalf of the Central Government of India. The currency is guaranteed by the Central Government, i. e. the use of a ten rupee note as a mode of payment is legal as per Indian laws, which cannot be refused by anyone, as a mode of payment. Reserve Bank of India promises to pay rupees 10 in every situation to the bearer, who has a ten rupee note. This creates trust in people.

Question 5.

Why do we need to expand formal sources of credit in India?

Answer:

Formal sources of credit in India are banks and cooperative societies. Following are the reasons which show the need to expand formal sources of credit in India –

- Formal sources of credit save people from moneylenders, traders and employers, who want to trap their borrowers in indebtedness.

- Everyone can get loans from banks at a cheaper interest rate, in comparison to informal sources of credit.

- Bank loan with lower interest rate increases the earnings of the borrower and they can easily repay their loan.

- These loans help borrowers to improve their living standards.

Question 6.

What is the basic idea behind the SHGs for the poor? Explain in your own words.

OR

Explain the role of self-help groups in the rural economy.

Answer:

SHGs stand for Self-Help Groups. The basic idea behind the SHGs for the poor is to provide credit facilities at a cheaper rate and also without much documentation process. SHGs organise rural poor, particularly, women, usually belonging to one neighbourhood. A typical SHG has 15-20 members who meet and save regularly. This saving may be ₹ 25, ₹ 100, or more than ₹ 100 per member. Members can take small loans from these SHGs.

![]()

The group charges very nominal interest on these loans. Most of the important decisions regarding savings and loan activities are taken by the group members. If the savings of these groups are regular, they become eligible for availing loan from the bank. The loan is sanctioned in the name of group and is meant to create self-employment opportunities. The basic idea behind these SHGs, is to make people financially strong and self-dependent.

Question 7.

What are the reasons why banks might not be willing to lend to certain borrowers?

Answer:

Following are the reasons why the banks might not be willing to lend to certain borrowers :

- Borrowers do not have any collateral to deposit in the bank as a security.

- Borrowers do not furnish proper documents.

- Borrowers are already caught in the hand of debt.

- Borrowers are not in a position to repay the loan in the given time.

Question 8.

In what ways does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

Answer:

The Reserve Bank of India supervises the functioning of formal sources of loans, such as banks and cooperative societies. The RBI monitors the banks, in actually maintaining cash balance. RBI sees that the banks give loans, not just to businessmen and traders, but also to small cultivators, small-scale industries, small borrowers etc. Periodically, banks have to submit information to the RBI, regarding how much they are lending, at what interest rate, to whom etc.

This is necessary so as to maintain equality of who receives the loans, as the aim is that all industries should grow. Even small-scale industries should be given the advantage of loans. As a result, the country’s economy will also grow. This monitoring also ensures that banks do not loan more money than they are supposed to, as such an action can creates a crisis situation.

Question 9.

Analyse the role of credit for development.

OR

Explain the role of credit for economic development.

OR

Describe the importance of formal sources of credit in economic development.

Answer:

Credit plays an important role in the development of a country. Both, people and nations, require credit for various economic activities. The credit helps industrialists in meeting working expenses and in production, in time. Therefore, their earnings increase. Various people take credit for various purposes like agriculture, business, establishing small-scale industries or goods trade. Thus, we can see that cheap and affordable credit is very beneficial for the development of any country.

Question 10.

Manav needs a loan to set up a small business. On what basis will Manav decide whether to borrow from the bank or the moneylender? Discuss.

Answer:

On the following basis, Manav will decide, whether to borrow from the bank or the moneylender:

(i) Rate of Interest: First of all, Manav will make a comparison between the rates of interest of both, the bank and the moneylender. Manav will prefer to take the loan from one, that offers a lower rate of interest.

(ii) Conditions for loan: Manav considers the terms and conditions for the loan of both – the bank, and the moneylender.

Manav will prefer the one that offers:

(a) easy terms and conditions,

(b) easy and affordable instalments,

(c) less paperwork, etc.

Manav would decide to take loan from the bank as it offers- a low rate of interest, simple terms and conditions, less paperwork, easy instalments etc.

![]()

Question 11.

In India, about 80 per cent of farmers are small farmers, who need credit for. cultivation.

(a) Why might banks be unwilling to lend to small farmers?

(b) What are the other sources from which the small farmers can borrow?

(c) Explain with an example how the terms of credit can be unfavourable for the small farmer?

(d) Suggest some ways by which small farmers can get cheap credit.

Answer:

(a) Banks might not be willing to lend to small farmers because they do not have collateral, as security, to deposit in the bank and appropriate documents. Some farmers are already caught in the hand of debt. Besides, some farmers do not repay their loans in time, due to the uncertainty of crops.

(b) The other sources, from which the small farmers can borrow, are – moneylenders, land-owners, traders, friends, relatives, self-help groups etc.

(c) The terms of credit can be unfavourable for small farmers. For example – a person takes a loan on a high rate of interest from informal sources like landlords, moneylenders etc., on behalf of the security of his land. At the end, if he or she is unable to pay the loan, due to a bad harvest, then the landlord or moneylender can sell his land to get his money back. In this situation, the loan pushes the farmers into a debt trap.

(d) Small farmers can get cheap credit from banks, co-operative societies and self-help groups and their rate of interest is also lower than the other sources of credit. The farmers can repay the loan easily after 4 or .5 years, or as decided before.

- costs of borrowing increase the debt burden.

- issues currency notes on behalf of the Central Government.

- Banks charge a higher interest rate on loans than what they offer on

- is an asset that the borrower owns and uses as a guarantee until the

Question 12.

Fill in the blanks :

(i) Majority of the credit needs of the …………… households are met from informal sources.

(ii) …………… costs of borrowing increase the debt-burden.

(iii) ………….. issues currency notes on behalf of the Central Government.

(iv) Banks charge a higher interest rate on loans than what they offer on ………….

(v) …………… is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender.

Answer:

(i) Poor

(ii) High

(iii) Reserve Bank of India

(iv) deposits

(v) Collateral.

Question 13.

Choose the most appropriate answer.

(i) In an SHG most of the decisions regarding savings and loan activities are taken by-

(a) Bank

(b) Members

(c) Non-government organisations

Answer:

(b) Members.

(ii) Formal sources of credit do not include –

(a) Banks

(b) Co-operatives

(c) Employers.

Answer:

(c) Employers.

![]()

Additional Project/Activity

(i) The following table shows people in a variety of occupations in urban areas. What are the purposes for which the following people might need loans? Fill in the column

| Occupations: | Reason for needing a loan: |

| 1. Construction worker | |

| 2. A graduate student who is a computer literate | |

| 3. A person employed in government service | |

| 4. Migrant labourer in Delhi | |

| 5. Household maid | |

| 6. Small trader | |

| 7. Autorickshaw driver | |

| 8. A worker whose factory has closed down |

(ii) Classify the people into two groups based on whom you think might get a bank loan and those who might not. What is the criterion that you have used for classification?

Answer:

(i)

| Occupations: | Reason for needing a loan: |

| 1. Construction worker | To buy essential tools and equipments for construction work. |

| 2. A graduate student who is a computer literate | To establish a computer centre. |

| 3. A person employed in government service | To buy a house or plot. |

| 4. Migrant labourer in Delhi | To buy a house. |

| 5. Household maid | To buy household items and for treatment of sickness. |

| 6. Small trader | To expand business. |

| 7. Autorickshaw driver | To buy a new autorickshaw. |

| 8. A worker whose factory has closed down | To meet his daily needs. |

Answer:

(ii)

| These people can get loans: | These people cannot get loans: |

| (i) Graduate student, who is computer literate. | (i) Construction worker. |

| (ii) A person employed in government sector. | (ii) Migrant labourer in Delhi. |

| (iii) Small trader. | (iii) Household maid. |

| (iv) Autorickshaw driver. | (iv) A worker whose factory has closed down. |

For classification, I have used following criterion:

(i) Proper documents,

(ii) Collateral for deposit in the bank against the loan.